Photo- Key Chinese shipping routes along China’s new maritime “silk road”

After debating whether it was about regime change, nuclear weapons, or the defanging of regional proxies, the United States and Israel’s war with Iran reached an impasse at the Strait of Hormuz.

That twist has refocused attention on the world’s oceans and their critical role in interconnected global commerce. Few of us can insulate ourselves from trade that funnels through just a handful of key choke points. It’s a lesson China knows well: For some 25 years, it has been buying and building ports across the Indian Ocean and Persian Gulf and around the world. The United States, meanwhile, is only now sitting up and taking notice.

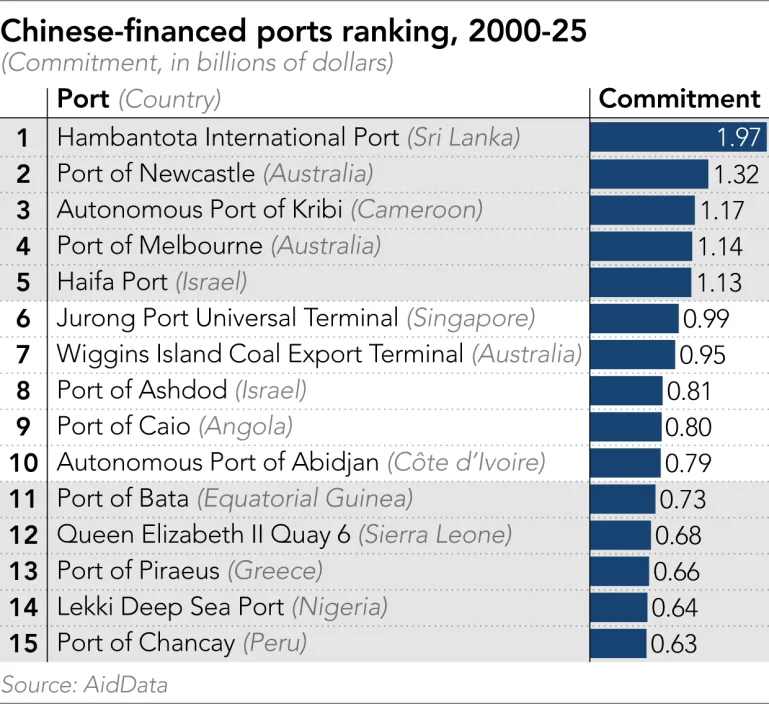

U.S. Ambassador to Greece Kimberly Guilfoyle recently suggested, for instance, that China should put up for sale the Greek port of Piraeus, a major shipping hub and gateway to southern Europe. It is not clear why China—which financed Piraeus, legitimately, a decade ago when Greece was in economic freefall and a hand up from Beijing was welcomed by virtually all parties—should give up the port. But it fits a pattern: The U.S., asleep for decades while China built a top-to-bottom maritime empire, is now trying to undo patient relationship-building by Chinese official agencies and state-owned entities in service of a vast network of overseas ports.

Besides Piraeus, the Trump administration brought pressure to bear in Panama over Chinese ownership of key ports there, and warned Peru that it will lose its sovereignty because of its relationship with China over the new mega-port of Chancay. And before the deal fell through, in 2024 the U.S. Development Finance Corporation (DFC) was going to back a half-billion-dollar port agreement in Colombo, Sri Lanka, to counter the Chinese-financed container terminal in the same location.

The U.S. has a long way to go if it wants to fight over every port China has financed: As we document in our new AidData report, Chinese agencies and state-owned enterprises (SOEs) have bankrolled some 363 Chinese loan- and grant-financed projects worth $24 billion supporting 168 unique ports across 90 countries from 2000 to 2025. The year 2000 is our data-collection starting point, as this was the beginning of the implementation of the state-led “Go Out” initiative, which encouraged Chinese agencies and SOEs to focus loans, grants, and investments in foreign countries rather than at home. Our underlying data presents an as-close-to-real-time picture of Beijing’s global port footprint as there is, including new and recent ports that have been proposed but are as yet unfunded. For every high-profile or contentious case like a Piraeus, there is a Chinese-financed, massive port that has been built in a Tema (Ghana), a Kribi (Cameroon), or the new loan we uncovered for the port of Muara, in Brunei.

For most of the world’s powers—including China, the United States, and the European Union—economic statecraft, domestic industrial policies, and national security are now more closely intertwined than we have seen since perhaps World War II. But China already has a head start.

While the U.S. has spent years speaking of an Indo-Pacific pivot, in practical terms—as events of the past few weeks have shown—it has been embroiled, seemingly single-mindedly, in the Middle East and immediate adjacent regions. China, meanwhile, has been patiently investing in all corners of the world, to its economic, diplomatic, and geopolitical benefit.

Early on, financing port construction or expansion was one way Beijing could invest its surplus dollar reserves and get an attractive financial return. Developing countries were hungry for infrastructure, with many Western or Western-led aid and lending institutions having gotten out of the construction business years earlier. China proved a willing and able partner.

But while news stories periodically appear describing the possible establishment of future overseas Chinese naval bases, we believe Beijing has evolved into a more sophisticated, subtle strategy. China is less focused on acquiring sovereign control of overseas territory, more so in assuring its own strategic security—built upon key points of access, or hubs of connectivity, conduits for trade, communication, data, capital, and influence. To this end, official Chinese financiers (government agencies and SOEs) increasingly co-locate their port investments with other investments, such as critical mineral sites. Low-visibility ownership with a commercial intent is also easier to defend than the physical footprint of a large military base. Access does not have to mean homeporting a couple of People’s Liberation Army Navy (PLAN) guided-missile destroyers; in the future, it could be as simple as a Chinese-owned and -operated overseas port with a Chinese police presence or perhaps a home for a commercial drone operation.

China continues to finance ports that can receive its vast exports as well as facilitate the importation of key commodities, such as soybeans, critical minerals, liquefied natural gas (LNG), oil, and more. These ports are designed to promote Chinese commercial interests overseas and maximize profits for its lenders—which we believe is largely the intent in Chinese-financed ports in the world’s wealthy countries. But in addition to financial returns, China gains influence, prestige, data. This focus on economic and commercial pursuits is happening at the same time that China’s navy is undergoing massive growth, both quantitatively and qualitatively.

China’s global maritime supply chains, anchored by Beijing’s overseas port network, provide a geopolitical benefit—a parallel logistic network that offers strategic independence free from interference from Western-led institutions—that permits China to contemplate a military counter to possible island chain containment strategies or constricting blockades attempted by an enemy in any future conflict. China has built and financed ports not just at maritime choke points, but all around them, including Panama. And so it’s no surprise that our data and analysis suggest that the higher the level of Chinese official economic involvement at a given port, the more likely it is to host some type of Chinese military activity—more than half the ports in our dataset with Chinese or Hong Kong ownership stakes have also hosted PLAN ship visits, for example.

The “port-park-city” model that worked so well domestically in China’s economic growth model decades ago has evolved into the “port-railway-mine” model. The Chinese, Tanzanian, and Zambian governments, for example, signed on in September 2025 to a $1.4 billion deal for the China Civil Engineering and Construction Corporation to rehabilitate the Tanzania-Zambia Railway project and its equipment, as well as to operate it. The transportation corridor will extend into mineral-rich Zambia, with a port terminus at Dar es Salaam, Tanzania. Increasingly, official Chinese-financed ports are mere jumping-off points for a growing set of inland supply lines, connecting land-locked regions to coastal cities.

https://e.infogram.com/_/OCnMJYgJaWiLOxFYVw2K?parent_url=https%3A%2F%2Fforeignpolicy.com%2F2026%2F04%2F15%2Fchina-ports-maritime-power%2F&src=embed#async_embed

In addition to offering relative speed, agility, and large sources of capital, China’s comparative advantage is in being able to provide a package of services to a client country. We found that approximately 35 percent of port and/or port facility projects financed by Chinese official-sector agencies also involve Chinese port ownership and/or operational control. Besides construction or expansion, a Chinese entity or series of entities might operate the port; furnish the massive shoreside cranes and the customs scanners; offer a free logistics platform; and bring in major shipping and logistics companies, with the latter ensuring the port is on major shipping routes and connected to global networks.

To be sure, there are potential negative aspects to this, for both port-hosting nations as well as China’s maritime rivals: Operating rights confer significant practical authority, including control over scheduling systems, berth allocation, logistics coordination, and day-to-day port management. This is the state of play at Piraeus. In many cases, Chinese SOEs that obtain operating rights are positioned to influence shipping routes, prioritize affiliated carriers, and adjust traffic flows in ways that align with broader commercial or Chinese foreign-policy objectives. When combined with ownership stakes, these operational roles can amplify leverage, deepen long-term commercial integration, and enhance strategic influence over maritime trade corridors.

China’s enormous market share in maritime manufacturing as well as provision of free logistics platforms like LOGINK and other software systems mean ports are dependent on a closed, integrated ecosystem of highly automated Chinese port-operating systems and hardware, written to Chinese standards; financed, designed, and operated by official Chinese entities; and effectively excluding products or services from rival countries or companies. So, China has obtained a digital and data advantage in the realm of global maritime competition, in addition to its lead in hardware like its number of ships.

https://e.infogram.com/_/MkyVebdg3pEA8cfnWNnz?parent_url=https%3A%2F%2Fforeignpolicy.com%2F2026%2F04%2F15%2Fchina-ports-maritime-power%2F&src=embed#async_embed

While the U.S. is newly energized and eager to stop other countries from giving away their ports—and, by implication, their sovereignty—to China, it has been less able to demonstrate what it has to offer instead. Beijing is providing other nations with infrastructure, capital, economic development, and trade—in short, prospects—while the United States sends darkly worded warnings.

In some ways this is a reflection of the United States’ maritime imbalance, which is vested almost exclusively in military strength, rather than commercial. The U.S. builds few merchant ships, has a relatively tiny civilian fleet, and faces serious challenges trying to rehabilitate ports and their infrastructure in the continental United States, never mind building or financing harbors overseas.

Meanwhile, the Strait of Hormuz is open, subject to Iranian approval. If military planners always expected that Iran would move against the strait if threatened or attacked, then Western navies do not seem to have been overly prepared for the eventuality. As first the Houthis (in the Red Sea) and now Iran have shown, choke points and the vital trade they carry are vulnerable to both symmetrical and asymmetrical threats; the latter can include drones, speedboats, and sea mines. But Britain withdrew its last standing naval presence in the Persian Gulf earlier this year, and the U.S. sent home its last conventional minesweepers just before the war started.

In contrast, China has doubled down in the region, commercially. Since 2018, Beijing has been a highly active lender across the maritime Middle East and especially in the Gulf countries. It has funded a container port at Khalifa in the United Arab Emirates, New Doha Port in Qatar, the Duqm port in Oman, and the port of Gwadar in Pakistan’s far west and on the approaches to the strait, to name just a few. “America’s Maritime Action Plan,” released by the White House in February 2026, summarizes steps the U.S. government has taken to recapture some semblance of maritime preeminence, mostly on shipbuilding. The EU also recently released a ports strategy of its own. But the national security and economic strategies of the U.S., EU, or India (which is a regional overseas port funder) are currently no match for China’s level of coordination or alignment.

China’s nearly ubiquitous presence in the world’s top ports means that the U.S. cannot insulate itself from Chinese supply chains, in either peacetime or conflict. It must be selective about where it chooses to compete and on what dimensions.

- A Chinese container ship is unloaded in the port of Hamburg, Germany, on Oct. 26, 2022.How China Uses Shipping for Surveillance and Control Beijing’s global maritime operations double as intelligence-gathering outposts. ARGUMENT | ELAINE DEZENSKI, DAVID RADER

- A Chinese Navy ship with bow number 629 sails near Escoda Shoal, as seen during a maritime patrol in the disputed South China Sea on June 7.Beijing’s Dominance of the South China Sea Is Not Inevitable Groupthink and short-termism are clouding judgments about these waters.

ARGUMENT | BEN BLAND, WILLIAM MATTHEWS

ARGUMENT | BEN BLAND, WILLIAM MATTHEWS

In response, some U.S. policymakers have become singularly focused on shipbuilding as the cure to the country’s seasickness. While critical, it is just one piece of the puzzle. As U.S. maritime administrator Stephen Carmel recently noted: “Shipbuilding does not lead to maritime power. Maritime systems do.”

China’s vast and coordinated lead in these systems, at global scale and mapped against its economic, trade, and national security priorities, cannot be turned back merely through U.S. threats and attempts at coercion or chastisement—including in third-party port-hosting countries where it may have declining influence. Over the course of three centuries, first Britain and then the U.S. built dominant global maritime-based empires on bedrock positive values like trust, reliability, accountability, and a sense of opportunity as well as law and order backed up by their respective navies. It matters less that these ideals could not always be achieved in practice. China, through its end-to-end maritime empire constructed over the course of a mere 25 years, seems to have learned this lesson and is applying it more effectively, at the moment, than its originators are. Its overseas global ports portfolio is the anchor point that guarantees for itself a high measure of strategic security and insurance in the face of potential coming storms.

In addition to offering relative speed, agility, and large sources of capital, China’s comparative advantage is in being able to provide a package of services to a client country. We found that approximately 35 percent of port and/or port facility projects financed by Chinese official-sector agencies also involve Chinese port ownership and/or operational control. Besides construction or expansion, a Chinese entity or series of entities might operate the port; furnish the massive shoreside cranes and the customs scanners; offer a free logistics platform; and bring in major shipping and logistics companies, with the latter ensuring the port is on major shipping routes and connected to global networks.

To be sure, there are potential negative aspects to this, for both port-hosting nations as well as China’s maritime rivals: Operating rights confer significant practical authority, including control over scheduling systems, berth allocation, logistics coordination, and day-to-day port management. This is the state of play at Piraeus. In many cases, Chinese SOEs that obtain operating rights are positioned to influence shipping routes, prioritize affiliated carriers, and adjust traffic flows in ways that align with broader commercial or Chinese foreign-policy objectives. When combined with ownership stakes, these operational roles can amplify leverage, deepen long-term commercial integration, and enhance strategic influence over maritime trade corridors.

China’s enormous market share in maritime manufacturing as well as provision of free logistics platforms like LOGINK and other software systems mean ports are dependent on a closed, integrated ecosystem of highly automated Chinese port-operating systems and hardware, written to Chinese standards; financed, designed, and operated by official Chinese entities; and effectively excluding products or services from rival countries or companies. So, China has obtained a digital and data advantage in the realm of global maritime competition, in addition to its lead in hardware like its number of ships.

While the U.S. is newly energized and eager to stop other countries from giving away their ports—and, by implication, their sovereignty—to China, it has been less able to demonstrate what it has to offer instead. Beijing is providing other nations with infrastructure, capital, economic development, and trade—in short, prospects—while the United States sends darkly worded warnings.

In some ways this is a reflection of the United States’ maritime imbalance, which is vested almost exclusively in military strength, rather than commercial. The U.S. builds few merchant ships, has a relatively tiny civilian fleet, and faces serious challenges trying to rehabilitate ports and their infrastructure in the continental United States, never mind building or financing harbors overseas.

Meanwhile, the Strait of Hormuz is open, subject to Iranian approval. If military planners always expected that Iran would move against the strait if threatened or attacked, then Western navies do not seem to have been overly prepared for the eventuality. As first the Houthis (in the Red Sea) and now Iran have shown, choke points and the vital trade they carry are vulnerable to both symmetrical and asymmetrical threats; the latter can include drones, speedboats, and sea mines. But Britain withdrew its last standing naval presence in the Persian Gulf earlier this year, and the U.S. sent home its last conventional minesweepers just before the war started.

In contrast, China has doubled down in the region, commercially. Since 2018, Beijing has been a highly active lender across the maritime Middle East and especially in the Gulf countries. It has funded a container port at Khalifa in the United Arab Emirates, New Doha Port in Qatar, the Duqm port in Oman, and the port of Gwadar in Pakistan’s far west and on the approaches to the strait, to name just a few. “America’s Maritime Action Plan,” released by the White House in February 2026, summarizes steps the U.S. government has taken to recapture some semblance of maritime preeminence, mostly on shipbuilding. The EU also recently released a ports strategy of its own. But the national security and economic strategies of the U.S., EU, or India (which is a regional overseas port funder) are currently no match for China’s level of coordination or alignment.

China’s nearly ubiquitous presence in the world’s top ports means that the U.S. cannot insulate itself from Chinese supply chains, in either peacetime or conflict. It must be selective about where it chooses to compete and on what dimensions.

In response, some U.S. policymakers have become singularly focused on shipbuilding as the cure to the country’s seasickness. While critical, it is just one piece of the puzzle. As U.S. maritime administrator Stephen Carmel recently noted: “Shipbuilding does not lead to maritime power. Maritime systems do.”

China’s vast and coordinated lead in these systems, at global scale and mapped against its economic, trade, and national security priorities, cannot be turned back merely through U.S. threats and attempts at coercion or chastisement—including in third-party port-hosting countries where it may have declining influence. Over the course of three centuries, first Britain and then the U.S. built dominant global maritime-based empires on bedrock positive values like trust, reliability, accountability, and a sense of opportunity as well as law and order backed up by their respective navies. It matters less that these ideals could not always be achieved in practice. China, through its end-to-end maritime empire constructed over the course of a mere 25 years, seems to have learned this lesson and is applying it more effectively, at the moment, than its originators are. Its overseas global ports portfolio is the anchor point that guarantees for itself a high measure of strategic security and insurance in the face of potential coming storms.

Foreign Policy